The UCHealth clinic on Prospect Road and Lemay Avenue in Fort Collins sees about 180 patients a day, and these days this means that at least 180 times a day since the beginning of the year, its patient representatives must recite a new line in their welcoming script:

“Have you been told about the surprise billing form?”

And more often than not, the reply is: “The what form?”

“It’s a new law in Colorado about surprise billing.”

The law, which went into effect Jan. 1, protects insured Colorado medical patients against surprise medical bills. Surprise billing essentially happens when you think you are using a medical service covered by contracts with your insurer — known as an in-network provider — when in reality the doctor or hospital is not included in your insurance network. You may have no idea this is the case until the bill for services comes, and “surprise!” you must cover that out-of-network difference in cost, which can add up to thousands of dollars.

The new protections were championed by Pueblo Democratic Rep. Daneya Esgar in what she calls “the biggest lift” of her career.

Under the new law, patients won’t have to pay more than their normal insurance costs for emergency services, even at an out-of-network hospital. Be warned, though: Any patient going in for a non-emergency visit who sees an out-of-network provider still could be the hook for the extra cost. Which is why, UCHealth patient access representative Pam Story says, the law requires the facility tell you up front of that possibility and of your possible financial responsibility along with asking you to sign a disclosure form explaining the new law.

“Most people are like, ‘huh, I had no clue [about the new law],’ Story says. “We’ve had a few negative responses, one or two people who don’t like the government and don’t like government bureaucracy have refused to sign, but overall, it’s been fine.”

Even if patients refuse to sign, the law says they still receive the new protections.

Esgar says she hadn’t realized how big the problem of surprise medical billing was until she started hearing from people who went to emergency rooms they thought were covered by their insurance. “And when you’re in ER, you have no time to ask everyone in the room whether they are in your insurance network… that’s not your concern. You think you are doing the right thing [by going to an in-network facility].”

But, she said, she heard from people hit by unexpected out-of-network charges who ended up with liens on their homes. “People said ‘how is this even legal?’ But it was.”

Her first effort at passage in 2018 failed in the face of pushback from hospitals, doctors’ groups and insurers. The second time around, she brought critics and supporters to the table to hammer it out. Esgar recalls that more than 45 amendments were proposed in a massive give-and-take.

The measure’s House co-sponsor was Republican Rep. Marc Catlin, a farmer who represents the southwest corner of the state and who is typically more involved in agricultural and water issues. He says he came to the issue in a fashion similar to Esgar’s: “I had a fella come into the office — it was just a coincidence he came in — but he was actually in Denver going to his mortgage lenders to borrow against his farm so he could pay the surprise bill he gotten. And that’s not the way the system should work. That was the thing that jolted me.”

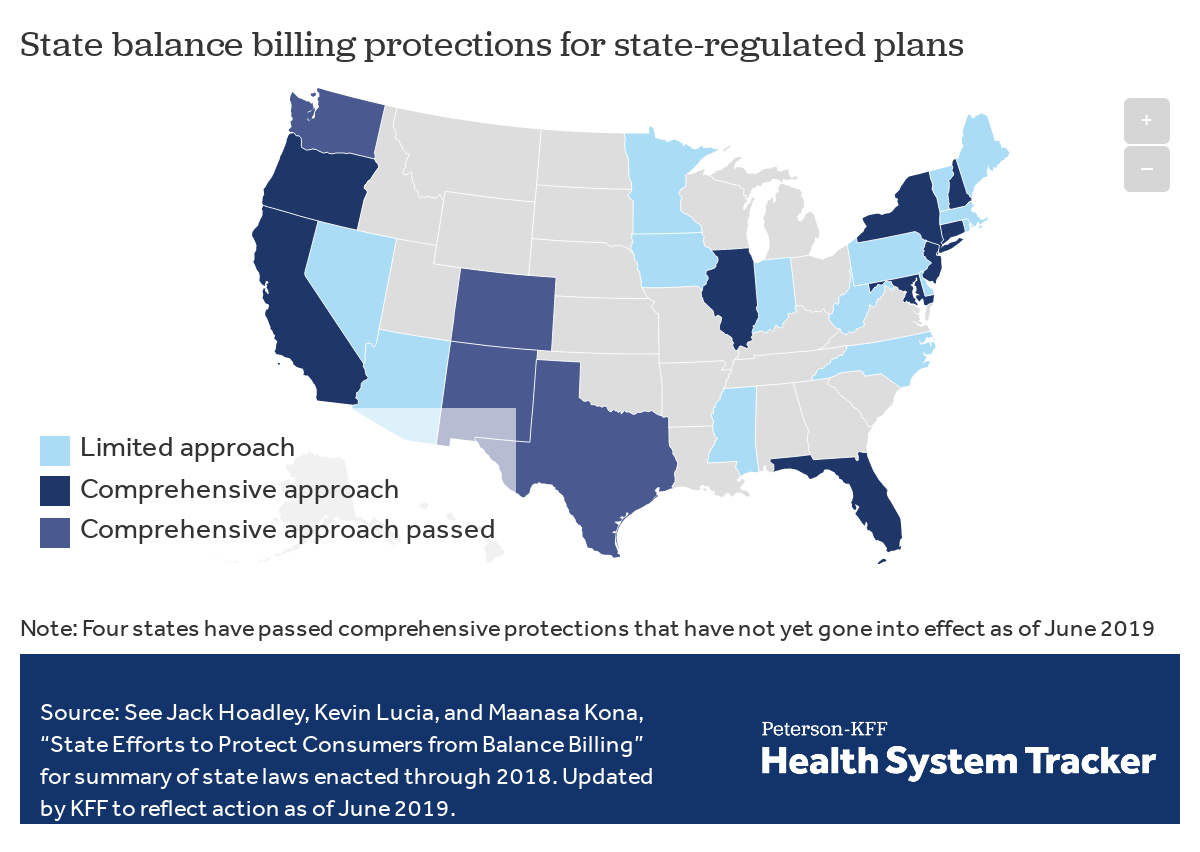

The Colorado Independent sought comment from the Colorado Medical Society and will update this story with its take on the new law when received. As of June 2019, at least 26 states, including Colorado, have passed laws to regulate surprise medical billing. California was one of the first states to create protections against surprise medical billing, with the law taking effect in 2017. Although it is too early to tell the larger effects of that law, a report from the insurance industry in the American Journal of Managed Care found that the number of doctors in California’s insurance network has actually increased since the law took effect, despite doctors’ groups in California arguing the law would disrupt medical care.

Meanwhile, in Washington, D.C., Colorado Democratic Sen. Michael Bennet is one of the authors of the bipartisan STOP Surprise Medical Bills Act, which was introduced in the U.S. Senate in 2019. That bill enacts national protections against surprise billing, but has been stalled since May.

Marcella Wells was among the patients at the UC Health clinic Wednesday morning. She said she’d heard something about surprise billing on a TV news spot “about someone who had gone into the ER and they ended with a bill from an anesthesiologist or some other person and it was a surprise billing. It was that kind of thing and it was like, ‘Whoa, that’s BS.’”

The law, she says, “is a step in the right direction,” though she said the disclosure form left her with more questions than answers and seems to rely not only on patients knowing the ins-and-outs of their policies, but also on insurance companies making sure their policy holders remain informed.

“My doctor sent me to see a nutritionist,” Wells says. “Well, is she in-network or not? If I went to urgent care or to a dermatologist, what is out-of-network for me…?”

“Examples would help. If you fall in the middle of the night, and you have to go to the emergency room, but maybe the closest ER is not in-network. So if it’s not, this is what will happen, and if it is, well, then this is what will happen.”

In Wells’ example, it does not matter under the new law if emergency services are in- or out-of-network, insurers can only bill a patient for the in-network cost — so no more surprise bills from that out-of-network anesthesiologist.

Here’s a simplified explanation of the new protections you now have as a patient under the law:

First, the new law requires medical providers to notify you of your rights under the law and a medical provider can’t force or coerce you to give up those rights.

The strongest protections are for patients seeking emergency services. Again, it won’t matter if the ER is out-of-network. The most you can pay for emergency services is the normal cost associated with your plan. So, if you are in a life-threatening situation you can go to the nearest hospital and not have the added worry of wondering if your insurance will cover the visit. It will.

The next level of protection involves visits to in-network facilities who may have health care providers that aren’t in-network working there. These facilities must tell you what kinds of services covered by your insurance might be provided by out-of-network providers. You have the right to request that someone in your insurance network provides that service. If the response is, ‘we don’t have someone in-network,’ you can receive covered services from another provider and cannot be billed for the out-of-network extra cost.

As Esgar puts it: “You are doing everything right, thinking you going to an in-network facility. Why should you be in the middle of the insurance company saying, ‘We’re not paying this much,’ and the doctor saying, ‘Well, this is what I charge.'”

Finally, out-of-network costs for emergency services or for covered services under the new law must count toward your deductible — the maximum amount you can pay per year before insurance covers the rest. If someone overpays for any medical services under the new protections, the provider is required to issue a refund within 60 days.

The Colorado Division of Insurance will hold a hearing on Feb. 4 to address details around how medical carriers disclose the new requirements of the law to patients.

[ad number=”2″]

[ad number=”5″]

{kind=link}

Good for Colorado for doing this, thank you M. Bennet and M. Catlin. Reminds me of when I was having a severe allergic reaction and my in network ER was 30 minutes away. I went to an ER that was 5 minutes down the road and was seen. Treated with IV solumedrol, pepcid and benadryl and was able to stop the reaction in its tracks. It was coded as a level 4 visit which my insurance company did not see as something it should cover since at that point it was non life threatening. Well, if I’d been driven up to my ER my airway would probably have been compromised, it was a bad reaction. So I averted a true medical emergency. I ended up having to pay the 1,000 ER visit out of pocket, my insurance would not pay! This law I think would have helped.

Thanks for the great article. I’m curious though, about what the rules are for issuing refunds for IN-network providers. I manage the billing for a clinic that has over-collected from patients – either because insurance came back and paid, or because a deductible was met during treatment, etc. – and now those patients have credit balances. The clinic does not prioritize sending money back to the patients, and in some cases the patients are unaware they are owed any money. This seems unethical and I’m trying to find any state laws I can point to that will maybe light some fires under the clinic management. Any help would be much appreciated!